July 10, 2020 Author’s Note: Two days after this article was published, the SEC proposed to update Form 13F and – most significantly – increase the reporting threshold from $100 million to $3.5 billion. As much as I would like to take credit for the SEC’s swift reaction to my article, I had nothing to do with it and the timing is pure coincidence. Naturally, this reporting threshold increase – if adopted – will dramatically decrease the number of advisory firms subject to Form 13F reporting. As of the date of this Author’s Note, the proposal is currently in a 60-day comment period. After the comment period expires, the SEC will either adopt the proposed Form 13F amendments as-is or with modifications, or will let the proposed amendments die on the vine without adoption. And just to be clear: the $100 million reporting threshold and all the attendant compliance obligations remain in effect until such time as Form 13F is formally amended by the SEC. With this additional context in mind, I have strived to insert additional Author’s Notes at various points in this article when appropriate to account for the potential (and hopeful) changes to Form 13F. Enjoy!

May 23, 2023 Author’s Note: Given that nearly three years have passed since the SEC originally proposed to increase the Form 13F reporting threshold from $100 million to $3.5 billion, I think it’s safe to say that the proposal has died on the vine and the reporting threshold will remain at $100 million for the foreseeable future.

* * * * *

During the first half of the 20th Century, institutions such as bank trust departments, insurance companies, investment companies, investment advisers, and other large market participants collectively underwent a secondary market trading spree, deploying their substantial capital to buy and sell securities of publicly traded companies that began to catch the attention of Congress after World War II.

This spree appeared to have the effect of concentrating financial marketplace dominance in the hands of a select few participants who owned a disproportionately large percentage of the available shares (and therefore could directly impact shareholder votes), thereby raising anti-competitive red flags. With respect to investment advisers alone, 24% of the industry’s collective assets under management in 1970 were concentrated in just five advisory firms. The largest 25 firms advised 60% of assets. The top 50 firms advised 76%.

Thus, in the summer of 1968, Congress directed the SEC to investigate the purchase, sale, and holding of securities by what it considered to be “institutional investors” in order to determine the effect of those activities on the maintenance of fair and orderly securities markets, the stability of those markets, and the interests of issuers of securities and of the public.

The directive was borne out of concerns regarding transparency and visibility into the investing activities of large market participants that could throw their relative weight around to negatively impact other market participants (and the public as a whole) since Congress didn’t know what it didn’t know; there was simply not enough data to support or reject the hypothesis that institutions and concentrated investment activity were detrimental to free markets and the investing public. Accordingly, the goal of the directed SEC study was economic rather than enforcement-oriented.

Congress’ concerns were validated when the SEC returned three years later with an Institutional Investor Study Report in 1971 that cited “gaps in information about the purchase, sale and holdings of securities by major classes of institutional investors” that were assessed by examining data that had never before been collected involving “trading activity, market impacts, and effects upon portfolio companies.”

As a result, the report recommended that the Securities and Exchange Act of 1934 (the “Exchange Act”) be amended to provide the SEC with general authority to require, on a continuous basis, reports and disclosures of securities holdings and transactions from all types of institutional investment managers.

And if you’re wondering why it took so long (three years!) for the SEC to complete the Institutional Investor Study Report, it’s because the SEC had to – get this – analyze the equivalent of 800,000 IBM cards (paper punch cards that were used to input data in early computers) in order to derive the data from institutional investors it was looking for!

Four years and who knows how many paper cuts later, Congress adopted Section 240.13f-1 of the Exchange Act in 1975, and the SEC followed suit by adopting Rule 13f-1 and Form 13F three years later in 1978. Form 13F requires all “institutional investment managers” with discretion over at least $100M in Section 13(f) securities (explained below) to disclose their equity holdings on a quarterly basis.

Author’s Note: As noted in the proposed amendments to Form 13F, Rule 13f-1 and Form 13F were originally structured such that “the burdens associated with filing Form 13F would be limited to ‘the largest institutional investment managers’”. Clearly that is not the case in today’s marketplace, as there are currently “5,089 managers that exceed the $100 million threshold file Form 13F holding reports. This is approximately 17 times the number of filers that the threshold covered in 1975.” To prevent the Form 13F reporting threshold from becoming once again “misaligned with the size and structure of the market and, as a result, place unnecessary reporting burdens on certain managers” in the future, the SEC is also proposing to revisit the reporting threshold every five years.

The goal of the newly created Section 13(f) in the Exchange Act (and SEC Rule 13f-1) was twofold: 1) create uniform reporting standards and a central repository of historical and current data about the investment activities of institutional investment managers (to be able monitor the role of institutional investors in public markets on an ongoing basis), and 2) inform public policymakers regarding the influence and impact of institutional investment managers on the securities markets (by analyzing the data that was being collected).

Investment advisers reading this article may be wondering why they should even care about Rule 13f-1, and Form 13F promulgated under the Exchange Act. After all, the primary bodies of law to which investment advisers are subject are the Investment Advisers Act of 1940 (for SEC-registered investment advisers) and the securities acts of the various states (for state-registered investment advisers), and the respective rules promulgated thereunder. And surely most advisers aren’t considered “institutional investment managers” given the advisory industry’s overall fragmentation and the growth of smaller independent advisory firms, right?

Author’s Note: Given the proposed increase to the Form 13F reporting thresholds, it seems the SEC would answer my rhetorical questions in the affirmative.

As this article will attempt to demonstrate, the net cast by Rule 13f-1 and Form 13F is much broader than what an independent advisory firm might think, and in particular with the recent industry shift towards ETF investing, far more RIAs are subject to the 13F reporting rules than most may realize.

How Exactly Does The SEC Define Section 13(f) Securities?

To quote Rule 13f-1 itself, section 13(f) securities means, in relevant part:

…equity securities of a class described in section 13(d)(1) of the [Exchange] Act that are admitted to trading on a national securities exchange or quoted on the automated quotation system of a registered securities association. In determining what classes of securities are section 13(f) securities, an institutional investment manager may rely on the most recent list of such securities published by the Commission pursuant to section 13(f)(4) of the Act (15 U.S.C. 78m(f)(4))

The general takeaway is that 13(f) securities mainly include U.S. exchange-traded stocks, shares of closed-end investment companies, and shares of exchange-traded funds. The SEC publishes a comprehensive list of 13(f) securities on a quarterly basis and posts them on their website the list is in PDF format and is currently over 500 pages long, there is a column of the list that indicates whether a particular security has been added or deleted since the previous quarter’s list to make it easier to simply see what’s changed).

As a practical matter, advisers can compare the SEC’s official list for the current quarter against their internal client holdings for purposes of assessing reporting obligations, a solution that is becoming available in a growing number of portfolio performance reporting systems (or retain an independent 13F analysis and reporting service to do this on their behalf as described below).

Institutional Investment Managers (Including RIAs) With $100M or More of 13(f) Securities Are Covered By SEC Rule 13f-1

As a threshold matter, Rule 13f-1 applies to “institutional investment managers” that manage $100M or more in certain types of securities, known as “section 13(f) securities”. As quoted above, Section 13(f) securities generally include equity securities that trade on an exchange (including the Nasdaq National Market System), certain equity options and warrants, shares of closed-end investment companies, and certain convertible debt securities. Notably, this means that ETFs are 13(f) securities as well, although mutual funds (which are open-end investment companies) are not.

In practice, most financial advisors may not automatically think of themselves as “institutional investment managers”. This is likely attributed to the fact that the term “institutional” had a much different meaning nearly a half-century ago than it does today. At best, the term hasn’t aged well since its original incorporation into Rule 13f-1 in 1978; at worst, it is a bit of a misnomer in present-day industry parlance. Nonetheless, when RIAs use 13(f) securities (like ETFs) in their portfolios, meet the $100M threshold, and “manage” client portfolios with discretion, they actually do meet the definition provided in the Exchange Act.

This is because the Exchange Act defines an “institutional investment manager” as “any person, other than a natural person, investing in or buying and selling securities for its own account, and any person exercising investment discretion with respect to the account of any other person.”

While the first category (including entity investors of their own accounts) is aimed at banks, insurance companies, broker-dealers, corporations, and pension funds that manage their own portfolios, the second category includes those investing on behalf of others and is aimed at discretionary investment managers (or potentially the trust department of a bank).

Importantly, this means that one does not necessarily even need to be registered with the SEC in order to be considered an institutional investment manager. The requirement is not being an SEC-registered investment advisor, but simply “any person exercising investment discretion with respect to the account or any other person”.

A person exercises “investment discretion” with respect to an account if, directly or indirectly, such person “is authorized to determine what securities or other property shall be purchased or sold by or for the account, or makes decisions as to what securities or other property shall be purchased or sold by or for the account even though some other person may have responsibility for such investment decisions.” Which, notably, covers not only solo ‘discretionary’ investment management by RIAs alone, but also effectively covers co-advisory arrangements (partially-delegated or shared investment management with another independent adviser) and sub-advisory arrangements (wholly-delegated investment management to another independent adviser).

In summary, the rules that make one subject to Rule 13f-1 are based on discretionary authority, the dollar value of assets under discretion, and the type of securities over which such discretionary authority exists.

The universe of advisers subject to Rule 13f-1 has undoubtedly expanded over the last 40+ years, and perhaps goes beyond the SEC’s original intent to simply encompass “institutional investment managers” that have the wherewithal to affect fair and orderly securities markets.

Today, a $100M+ adviser managing discretionary ETF portfolios for its clients is not exactly uncommon. In fact, the Rule’s reach has significantly expanded further by the growth of the ETF universe, and the ever-increasing market share that ETF sponsors command in comparison to mutual funds – which is notable because again mutual funds are not 13(f) securities, but ETFs are, such that the shift of advisory firms from the former to the latter is causing a broad swath of them to suddenly become “institutional investment managers” of 13(f) securities.

In other words, when one combines the overall growth of the financial advisor industry, and the expansion of the AUM model and its discretionary management services, with the growth of ETFs – and the fact that the $100M threshold has remained unchanged since 1978 – Rule 13f-1 should be on more advisers’ minds if it isn’t already.

Form 13F Requires Advisors To Report Details About Their Equity Holdings On A Quarterly Basis

Technically there are actually three different versions of the SEC’s Form 13F. How another institutional investment manager may exercise discretion over the same 13(f) securities as the reporting institutional investment manager will dictate which form to use, as follows:

- A “Holdings Report” is utilized if all of the reporting institutional investment manager’s 13(f) securities are reported on its own Form 13F (e.g., RIAs with no co-advisory or sub-advisory relationship with another independent investment adviser);

- A “13F Notice” (Form 13F-NT) is utilized if all of the reporting institutional investment manager’s 13(f) securities are reported on Form 13F by another institutional investment manager (e.g., if the reporting adviser is in a sub-advisory relationship with another independent investment adviser);

- A “Combination Report” is utilized if only part of the reporting institutional investment manager’s 13(f) securities are reported on Form 13F, and the rest are reported by another institutional investment manager (e.g., if the reporting adviser is in a co-advisory relationship with another independent investment adviser).

These different versions are used essentially to avoid duplicate information being reported and to account for co-advisory or sub-advisory manager relationships.

Depending on which version of Form 13F is ultimately utilized as described above, the institutional investment manager will need to include a cover page, a summary page, and/or an information table. The Form 13F Instructions and Form 13F FAQs provide extensive details about how each form should be completed.

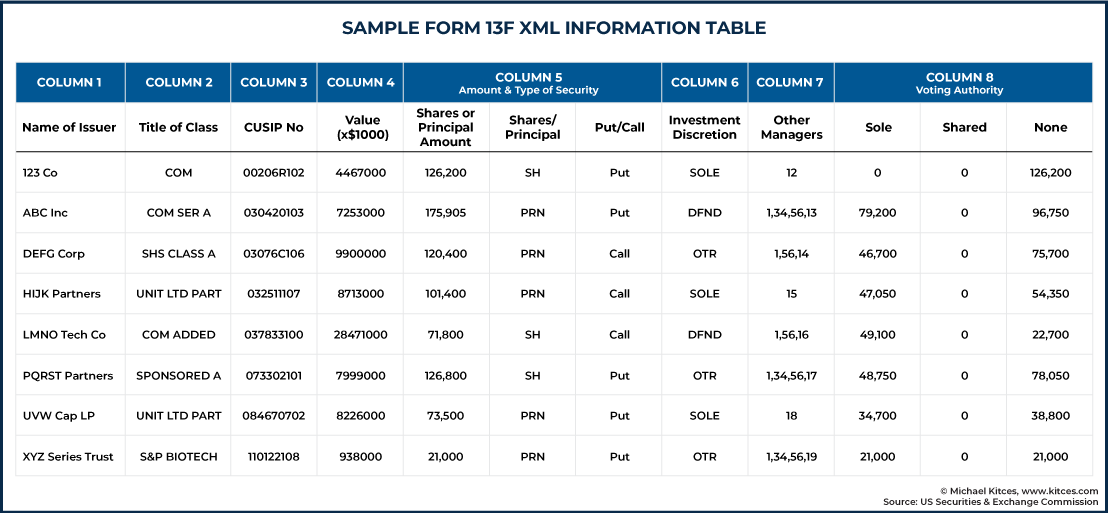

The information table is the meat of this filing sandwich, as it calls for descriptions of the actual security positions to be reported in an eight-column XML file (more on this file format later). For an example of what an XML information table should look like and instructions on how to create one using Excel, refer to the SEC’s Quick Reference Guide.

More specifically, the information table requires the following for each 13(f) security:

- Name of The Issuer

- Title of Class

- CUSIP Number

- Market Value (rounded to the nearest one thousand dollars)

- Amount and Type of Security

- Investment Discretion

- Other Managers

- Voting Authority

The first three columns (issuer name, class title, and CUSIP) are self-explanatory and are essentially copied directly from the SEC’s list of 13(f) securities as applicable.

When reporting market value, the value of the particular security is measured as of the last trading day of the calendar quarter and should only represent the security’s gross long-only value (i.e., exclude short positions and do not net out short positions).

Holdings may be omitted if fewer than 10,000 shares of a single issue are held, and the aggregate fair market value of holdings in the same issuer is less than $200,000 (effectively a de minimis threshold).

Author’s Note: In the proposed amendments to Form 13F, this de minimis threshold would be eliminated.

The “Amount and Type of Security” column generally requires the number of shares and an indication of whether the position represents a put or call option.

The “Investment Discretion” and “Other Managers” columns are intended to capture sole or shared investment discretion responsibility with others, and the “Voting Authority” column should indicate whether the filer exercises sole, shared, or no voting authority.

The Form 13F Instructions and Form 13F FAQs go into a lot more detail and should be reviewed in their entirety for further elaboration.

Author’s Note: The proposed amendments to Form 13F add a few data points to the form, including the CRD number / SEC filing number for the filing firm and any other manager included on the List of Other Managers Reporting for this Manager table on the cover page.

What Are The Initial & Ongoing Filing Deadlines For Form 13F?

If, on the last trading day of any month, an adviser exercises discretionary authority over accounts holding at least $100M of 13(f) securities, Rule 13f-1 kicks in, and four consecutive quarterly Form 13F reports must thereafter be filed.

The inaugural Form 13F need not be filed with the SEC, however, until 45 days after the last day of the calendar year in which the adviser first crossed the $100M threshold.

For example, if an adviser has $100M in 13(f) securities under discretion as of the end of March 2020, then 2020 is the first calendar year the advisor crossed the threshold, which means the advisor need not file their first 13F report until February 16, 2021 (the 45th day falls on a Sunday and the 46th day falls on a holiday (Presidents’ Day), so the deadline is technically the 47th day after the year-end).

The remaining three consecutive quarterly Form 13F reports must be filed within 45 days after the last day of each of the first three calendar quarters. Continuing the example above, the adviser must thereafter file its 2nd, 3rd, and 4th quarterly 13F reports by May 17, 2021, August 16, 2021, and November 15, 2021, respectively. All four quarterly 13F reports must be filed in 2021, even if the adviser dips below the $100M threshold.

If the same adviser again exercises discretionary authority over accounts holding at least $100M of 13(f) securities on the last trading day of any month in 2021, it will be required to file a total of four quarterly 13F reports in 2022 with the same sequence as above. Notably, the rule does not require that the advisor finish the 2021 year with $100M or more of 13(f) securities to be required to file in 2022; exceeding the threshold at the end of any month in 2021 is sufficient to trigger the filing obligation for all four quarters in 2022.

The Challenges Of Preparing And Filing Form 13F Via EDGAR

Once an RIA has met the 13F filing requirements by exceeding the $100M threshold in 13(f) securities for any month… the fun really begins in trying to figure out how exactly to file Form 13F for the first time.

As alluded to above, the information table of the Form 13F must be prepared in Extensible Markup Language or “XML” format, which is a specific machine-readable electronic format that… well, let’s just say you can’t necessarily download an Excel file from your custodian and call it a day. Though some manipulation of an Excel file from your portfolio management software provider can do the trick, any errors in the resultant XML file will be rejected by the SEC as part of the attempted filing process.

The SEC has published a 33-page Form 13F XML Technical Specifications instruction manual of sorts, which also includes accompanying XML stylesheets, samples, and schema files for institutional investment managers’ perusal. This instruction manual just covers the XML formatting process for Form 13F’s information table; we haven’t even addressed the actual filing process through the SEC’s Electronic Data Gathering, Analysis, and Retrieval (“EDGAR”) system, which is a separate beast in and of itself!

Suffice it to say, even the SEC suggests that the average adviser may need help preparing a Form 13F submission: “The expectation is that software developers, working on behalf of filers, will be able to construct software that will generate a Form 13F submission that can be successfully processed by the EDGAR system.” This statement can be interpreted to suggest that the preparation and filing process of Form 13F is complicated enough to justify hiring a tech vendor to do it for you.

With some time, energy and effort, though, advisers themselves can certainly conform an XML file for submission to the SEC through EDGAR; the SEC even provides instructions on how to create an XML information table from an Excel file.

Filing of Form 13F is accomplished through the SEC’s EDGAR system, and getting credentialed to file information through EDGAR isn’t exactly a walk in the park either.

At a high level, getting credentialed to file with EDGAR involves uploading a notarized “Form ID” application, obtaining a central index key or “CIK” number, and setting a passphrase, password, and password modification code (collectively the “access codes”). The SEC will typically review the Form ID in two business days and respond with an acceptance. A detailed overview of the process, as well as answers to certain frequently asked questions, can be found on the SEC’s Filer Information website.

Once a new filer account is approved and fully established, the task now turns to actually figuring out how to use the EDGAR system and submit information to the SEC through it. There is an EDGAR Filer Manual specifically designed to guide filers through this process; however, the manual is a massive document comprised of two PDF volumes totaling over 1,000 pages (Volume 1 and Volume 2).

For those that are keen to outsource, there are a number of software vendors and technology consulting firms that specialize in extracting, scrubbing, formatting, and uploading Form 13F data. This can save a significant amount of time, especially considering that formatting the Form 13F data is only half the battle.

Firms such as File|13F by WealthFluent LLC, Securex Filings LLC, FilePoint, and maybe even an advisor’s own legal counsel or compliance consultant can save a lot of time and technical frustration by offloading the heavy-lifting and guiding advisors through the entire process.

The overarching point to be conveyed here is that it is basically impossible to condense the totality of the SEC’s XML formatting and EDGAR filing instructions into a digestible article whose length doesn’t cause readers’ heads to explode. I’ll leave the head-exploding responsibility to SEC’s XML/EDGAR instructional authors.

One important footnote to the filing process: an institutional investment manager can submit a request for confidential treatment as part of its Form 13F filing:

- If the information filed would identify securities held by a natural person, an estate, or a personal trust (known as the personal holdings exemption);

- If it is in the public interest or for the protection of investors, and at least one of the nine exemptions provided for in the Freedom of Information Act is satisfied (typically related to the protection of “trade secrets and commercial or financial information obtained from a person and privileged or confidential”); or

- Related to open risk arbitrage positions. More information about confidential treatment requests can be found in the Exchange Act, Form 13F instructions, and Form 13F FAQs.

For RIAs Managing $100M or More Of ETFs (Or Stocks) Who May Have Inadvertently Missed Prior Form 13F Filings

Some financial advisors may be reading this article and asking themselves, “I didn’t even know about Form 13F until reading this article, and probably should have been filing Form 13F for some time… what do I do now?”

The SEC’s Form 13F FAQs are only moderately helpful here, as FAQ #26 states, “We do not grant any extensions, so you should not call and ask for one or write us a letter explaining that your filing will be late. You should submit your filing as soon as possible after the filing deadline. You should not submit a misleading or incorrect filing.” Ignorance of a regulatory requirement is no excuse.

The most commonly-cited SEC enforcement action involving delinquent Form 13F filings is In the Matter of Quattro Global Capital, LLC, Rel. IA-2634 (August 15, 2007), in which a large hedge fund manager failed to submit any Form 13F filings for almost 4 years – and only initiated its first Form 13F filing after the SEC brought the matter to the manager’s attention in the course of an examination. Ultimately, Quattro agreed to be censured, to cease-and-desist from current and future violations, and to pay a $100,000 civil monetary penalty in its settlement with the SEC.

The SEC cited the fact that the manager’s compliance manual referenced Form 13F filing obligations, and that it had received several Form 13F filing advisories from its legal counsel and auditors. The real nugget from this enforcement action, however, is the reference to “retrospective Forms 13F” that the manager subsequently filed to catch-up on its delinquent filings.

The key takeaway here is that making late 13F filings is still better than making no 13F filings at all (and potentially just further compounding the period of non-compliance!), and waiting for the delinquency action to come to a head in the course of an SEC examination or enforcement action is not likely an improvement. And with use of ETFs and discretionary trading by RIAs on the rise, it may only be a matter of time before the SEC more proactively emphasizes enforcement in this area, given growing concerns of potentially-widespread RIA non-compliance.

The Past and Future of Form 13F ‘Paperwork’ Now Via XML

The formatting, filing, and SEC review of Form 13F data has evolved over the years. As a case in point, the SEC just transitioned from an old text-based ASCII format to the current XML format in 2013. At least part of the reason for this transition was a 2010 Report of the SEC’s Office of Inspector General (OIG) – Office of Audits, entitled “Review of the SEC’s Section 13(f) Reporting Requirements.” In it, the OIG minced no words in criticizing the SEC’s fundamental failure to actually do anything with the voluminous Form 13F data it received:

Significantly, our review found that despite Congressional intent that the SEC would be expected to make extensive use of the Section 13(f) information for regulatory and oversight purposes, no SEC division or office conducts any regular or systematic review of the data filed on Form 13F. We found that while IM [the Division of Investment Management] has delegated authority to grant or deny confidential treatment pursuant to Section 13(f), no SEC division or office has been delegated authority to review and analyze the 13F reports, and no division or office considers this task as falling under its official responsibility. […] No SEC division or office monitors the Form 13F filings for accuracy and completeness. […] The current text file format of Form 13F limits the facility to extract, organize and analyze the data being reported.

The OIG’s report gave advisors who toiled over many quarters of Form 13F filings – and incurring personnel and technology costs along the way – reason to be frustrated over the acknowledgment that the information they submitted was never reviewed or analyzed.

In an even more exasperating revelation, the SEC had apparently outsourced the preparation of the official list of Section 13(f) securities to a third-party vendor based on specifications last conveyed in 1979, did not review any of the third-party vendor’s work product, and had no contract or agreement in place with the third-party vendor.

The OIG went on to make 12 specific recommendations to improve the SEC’s utilization of Form 13F data. Besides telling the SEC to actually review the information it receives, it encouraged the adoption of a “more structured format that will make the data easier to extract and analyze,” and to re-analyze the impact of increasing the reporting threshold of $100M.

The former recommendation led to the transition from ASCII to XML, but the latter recommendation has not resulted in any increase to the $100M threshold (at least not yet). This $100M threshold has been in place since the rule’s adoption in 1978, and in this author’s humble opinion, it is high time that it be increased to only capture what are truly “institutional” investment managers per the SEC’s original intent. (Author’s Note: Ask, and you shall receive. )After all, if the threshold were simply adjusted for inflation alone, it would have risen from $100M to $413M today (as determined by the Bureau of Labor Statistics CPI Inflation Calculator); and even then, many would argue that RIAs of that size aren’t really large enough to be “institutional” managers that are capable of materially impacting the markets (as monitoring for such was the original purpose of 13F filings in the first place.).

Author’s Note: The proposed increase to the reporting threshold from $100M to $3.5B was not pulled out of a hat. The SEC arrived at $3.5B by “reflecting proportionally the same market value of U.S. equities that $100 million represented in 1975, the time of the statutory directive. The new threshold would retain disclosure of over 90% of the dollar value of the holdings data currently reported while eliminating the Form 13F filing requirement and its attendant costs for the nearly 90% of filers that are smaller managers.” I like this logic better than a pure inflationary adjustment.

An even deeper dive into the reliability of Form 13F filings is provided in the 2016 article entitled “Form 13f (Mis) Filings,” by Professors Anne M. Anderson and Paul Brockman, as posted to the Harvard Law School Forum on Corporate Governance website. The authors ultimately conclude that, “Instead of being a repository of reliable data that serve to ‘increase investor confidence in the integrity of the U.S. securities markets,’ our empirical results are consistent with investor complaints that ‘Form 13F filings are just a non-standardized mishmash of jumbled (and often inaccurate) information.’” In a nutshell: garbage in, garbage out.

Regardless of whether 13F data is actually reviewed or consistently reliable to begin with, any member of the public has access to Form 13F filings by simply searching for the filer’s name using the SEC’s EDGAR Search Tool.

Concluding Recommendations

Author’s Note: With time, let’s hope that these Concluding Recommendations apply to a lot fewer of the advisors reading this article.

While the Form 13F reporting requirements were originally created for “institutional investment managers” potentially capable of impacting markets or directly influencing companies – not exactly what most envision with an individual RIA managing client portfolios – the reality nonetheless is that any RIA managing $100M or more of 13(f) securities (including stocks and ETFs) with discretion is required to file Form 13F.

For advisers that are close to the $100M discretionary threshold of 13(f) securities, it is best to institute a new compliance checkpoint to confirm month-end assets under discretion going forward and prepare for the Form 13F filing obligations that will likely follow. Depending on the volume of client inflows, and especially considering the recent dramatic swings in markets, advisors will not want to be caught off guard by a month-end spike in discretionary assets under management that triggers four 13F filings in the subsequent year.

For those who will become subject to the 13F rules for the first time, be sure to explore existing functionality that may already exist through your portfolio management platform (e.g., Orion’s Compass App), as advisors may quickly realize that they already have helpful Form 13F analysis tools already at their fingertips to help generate the required XML files for submission to the SEC, and didn’t even know it.

And for those RIAs who may just now be discovering their 13F reporting obligation – and that they’ve been subject to it already for some period of time and weren’t submitting the reports as they didn’t even know – as the Quattro case demonstrates, the best time to start preparing for future Form 13F filings (or catching up on missed Form 13F filings) is now. Fortunately, though, a growing number of technology tools and service providers are available to help!

* * * * *

This article originally appeared in Michael Kitces’ Nerd’s Eye View on July 8, 2020.

You must be logged in to post a comment.