Welcome to the December 12, 2024 edition of On The Docket, which includes the following content:

- Two examples of impermissible hedge clauses

- “Unregistered broker activity” can result in SEC administrative proceedings

- A deeper dive on Form 13F filing requirements

- The Publisher’s Exclusion was recently challenged in a Federal District Court, and survived.

- Third-party ratings and testimonials compliance: the SEC is not messing around

- Did you know you can self-monitor your IAR Continuing Education progress with a FinPro Account?

- The scale of ‘off-channel communications’ penalties handed down by the SEC since 2021 is pretty staggering – $2 billion collected from over 100 firms

- Out of curiosity, I asked ChatGPT, Perplexity, Claude, and Gemini a question that I’m commonly asked:

- SEC Chair Gensler to depart on January 20, 2025; former SEC Commissioner Paul Adkins nominated as the new SEC Chair

- Seeking Best Execution: Understanding The SEC’s Expectations For Advisors To Deliver Best Outcomes For Clients

🌐 All past On The Docket editions (as well as other article, video, and podcast content) are available by visiting the On The Docket page of the Beach Street Legal website.

📥 If this edition was forwarded to you, you can subscribe directly by clicking here.

💬 Prefer to follow along via social media? You can follow us below:

- Twitter / X

- YouTube (more to come)

Happy reading.

– Chris

* * * * *

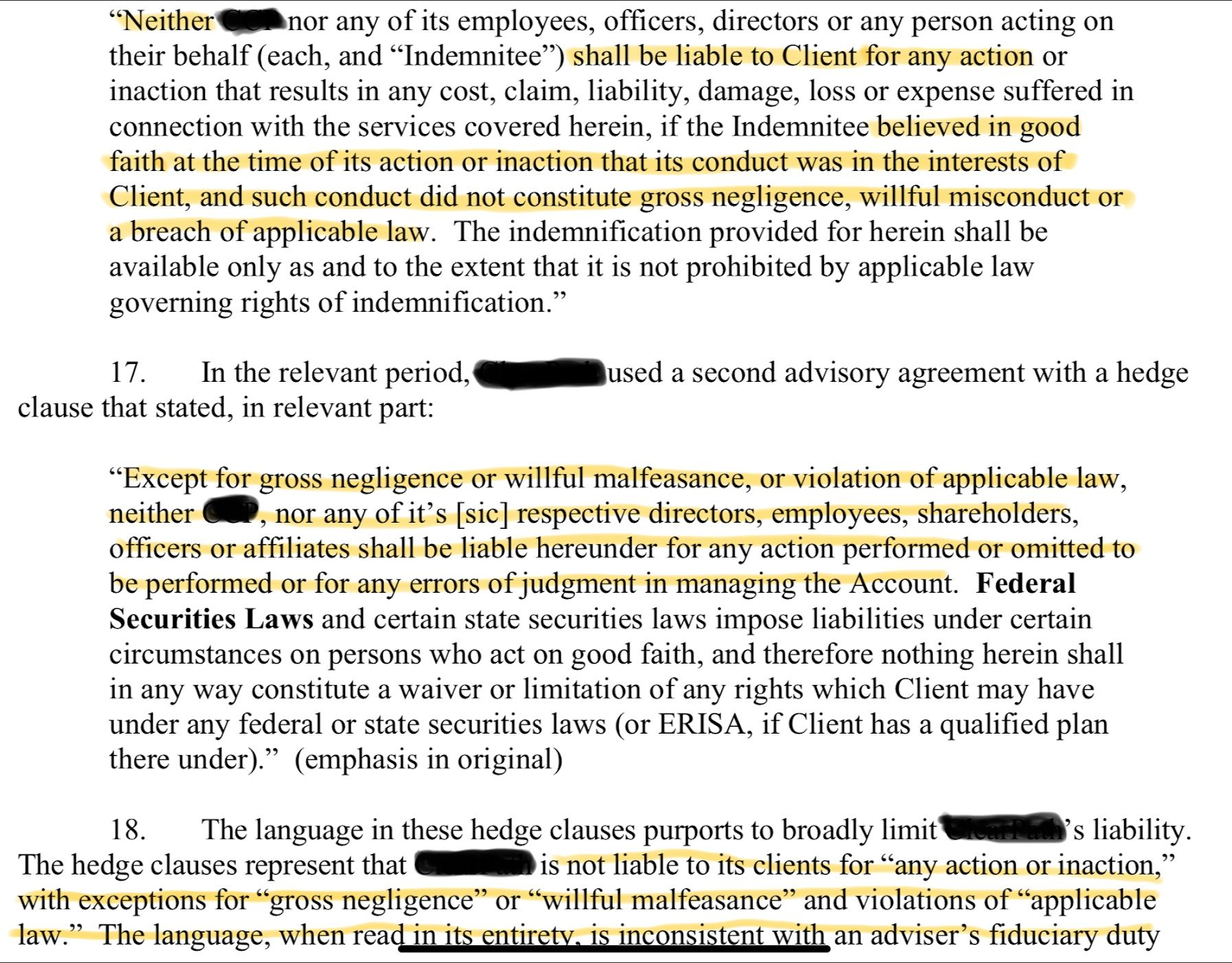

Two examples of impermissible hedge clauses

The annotated screenshot below is excerpted from a recent SEC enforcement action, and provides two helpful examples of what the SEC considers to be impermissible “hedge clauses” (Clauses in an advisory agreement that purport to limit an adviser’s liability to “gross negligence” or “willful misconduct” or that otherwise absolve an adviser of liability for “any action or inaction”):

Also – a “savings clause” that asserts that such liability limitations do not limit or waive a client’s rights under state or federal law is not enough to overcome the prohibition against such hedge clauses.

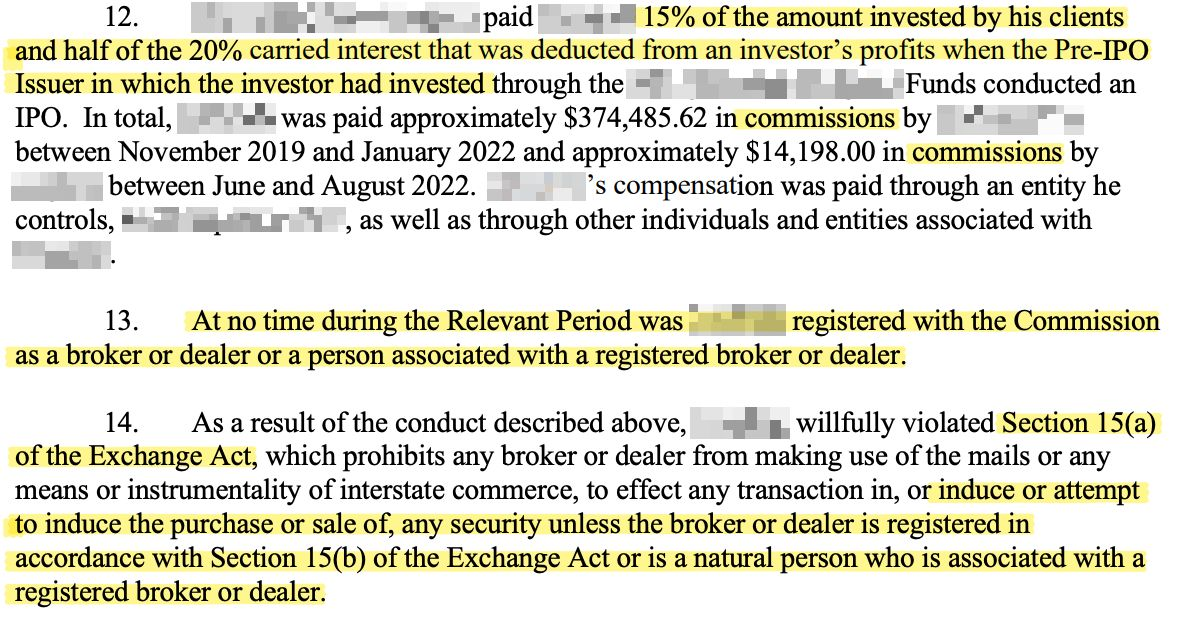

“Unregistered broker activity” can result in SEC administrative proceedings

In a recent trio of cases, three individuals “allegedly provided investors with marketing materials [of private investment offerings], advised investors on the supposed merits of the [private investment offerings], and received transaction-based compensation [from the private investment offerings’ sponsors, structured as a % of the amount invested by the individuals’ clients].”

As the SEC press release noted in the screenshot excerpt below, such activities are “hallmarks of a broker” and require registration as such.

Advisers (and everybody, really) should bear this in mind if a private fund sponsor offers to pay you an amount tied to the amount invested by your clients or otherwise due to your fundraising efforts.

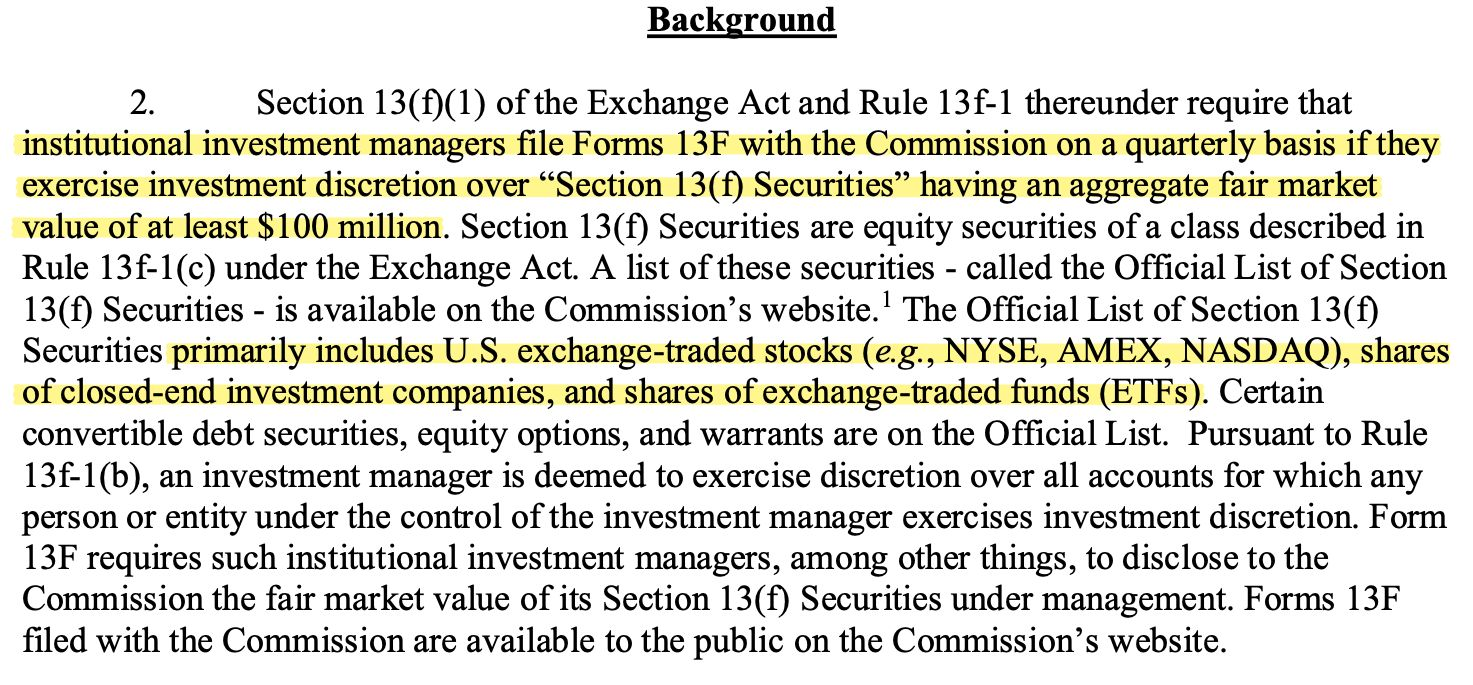

A deeper dive on Form 13F filing requirements

At first glance at these SEC enforcement actions as excerpted in the screenshot below, most advisers may think they’re not “institutional investment managers” and therefore do not have a Form 13F filing obligation.

However, an “institutional investment manager” includes any adviser that exercises investment discretion over at least $100M in Section 13(f) securities.

Section 13(f) securities include US exchange traded stocks and ETFs (among certain other securities), but NOT open end mutual funds.

For a deeper dive on Form 13F filing requirements, check out my prior article from 2020 here.

The Publisher’s Exclusion was recently challenged in a Federal District Court, and survived.

The case at hand was against Seeking Alpha, a freemium subscription-based website that provides tools and resources related to various publicly traded equities. The plaintiff subscribers alleged that Seeking Alpha should be registered as an investment adviser. Seeking Alpha contended that it was excluded from registration as an investment adviser under the Publisher’s Exclusion and precedent set by the Supreme Court in Lowe v. SEC.

Seeking Alpha prevailed.

More specifically, the court determined that SA’s subscription features:

☑️ Are not personal communications

☑️ Do not contain false or misleading info

☑️ Do not tout any security in which SA has an interest

☑️ Are bona fide

☑️ Are of regular and general circulation

☑️ Are advertised and sold in an open market

☑️ Are updated regularly

The decision also reminds us that Congress was “plainly sensitive to First Amendment concerns” in passing the Investment Advisers Act of 1940, and “did not seek to regulate the press through the licensing of nonpersonalized publishing activities”.

Also – importantly – a website feature that merely allows subscribers to filter generally available content is not enough to create personalized advice. Auto-trading features likely would not have survived similar scrutiny.

I wrote about investment adviser registration determinations in this linked article (including the Publisher’s Exclusion).

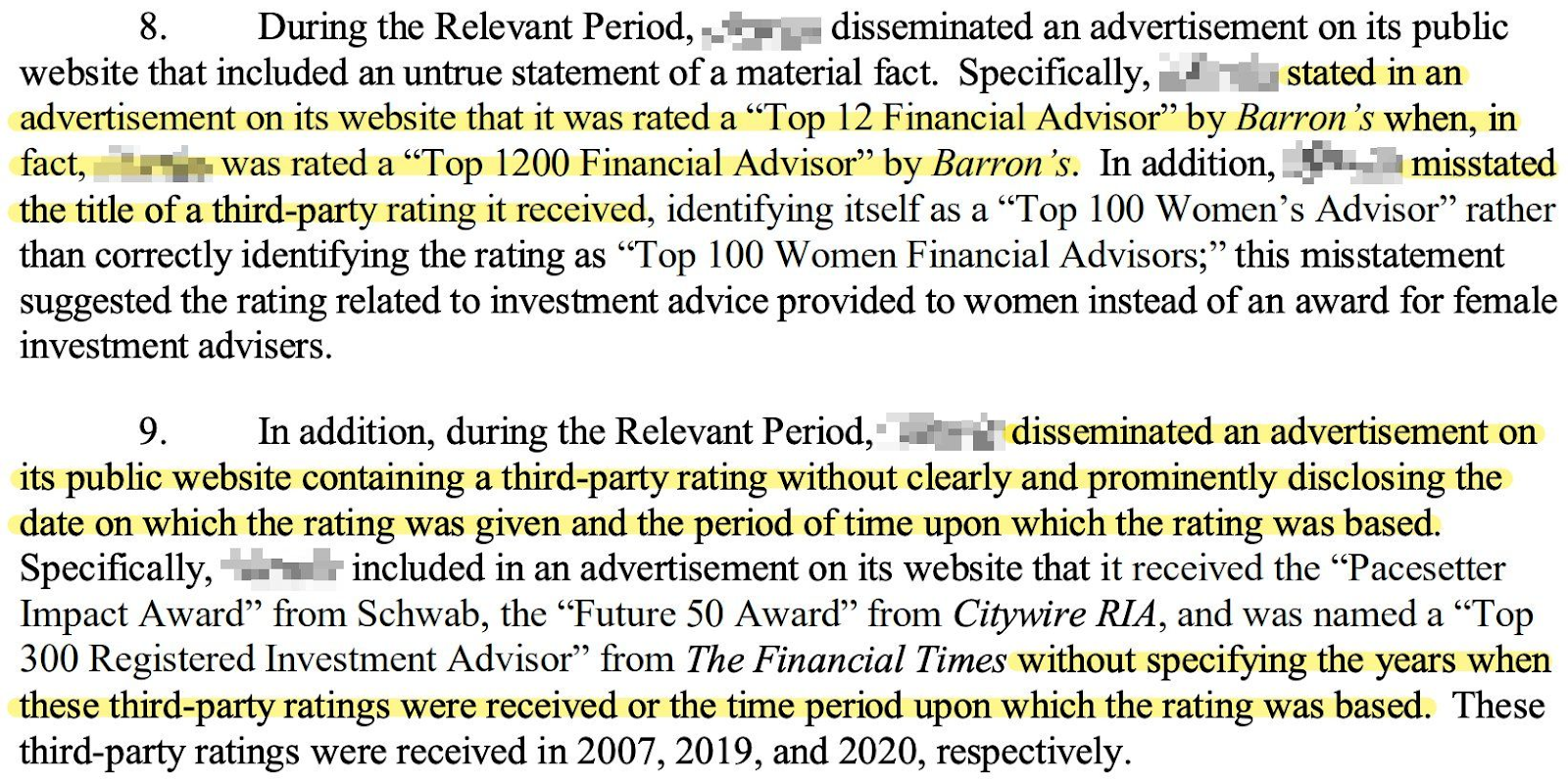

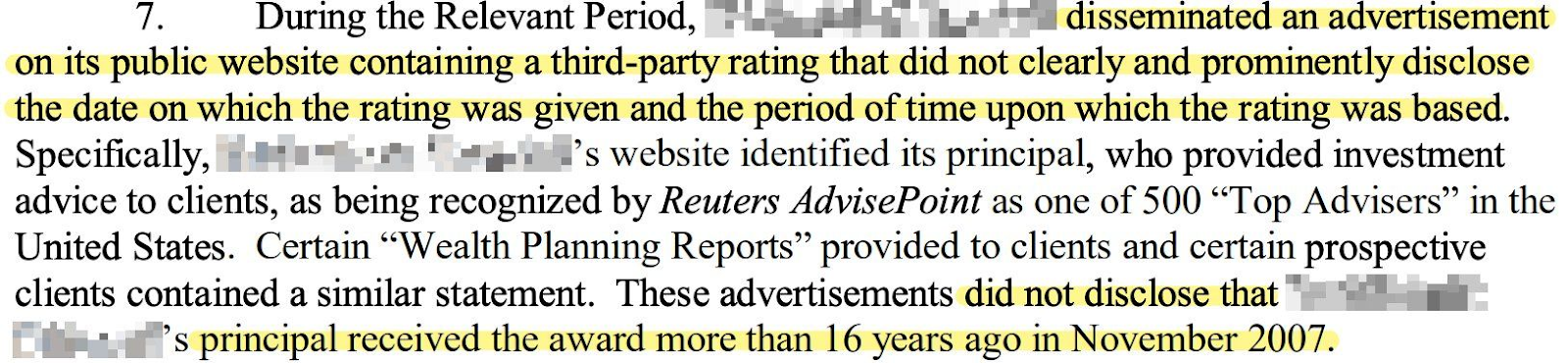

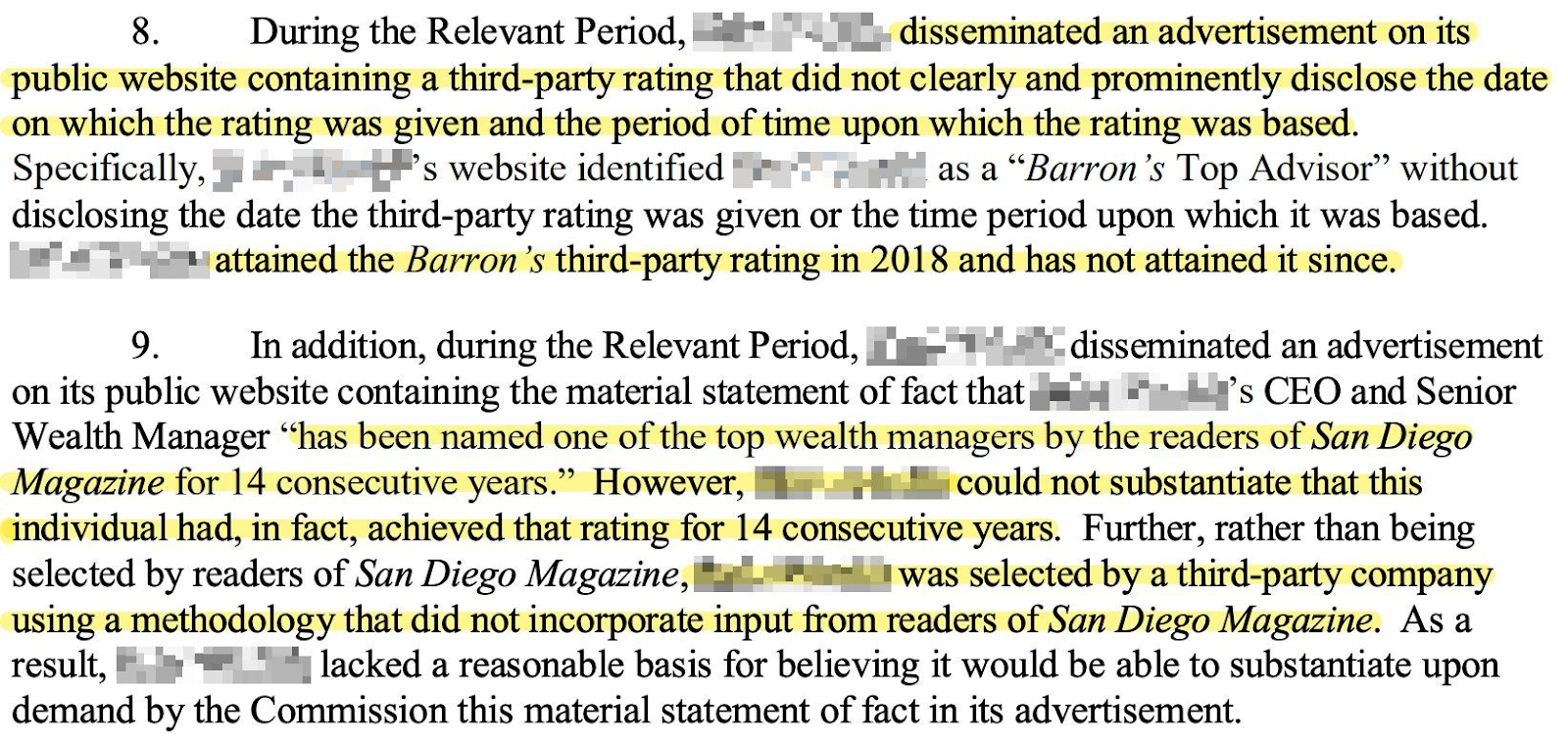

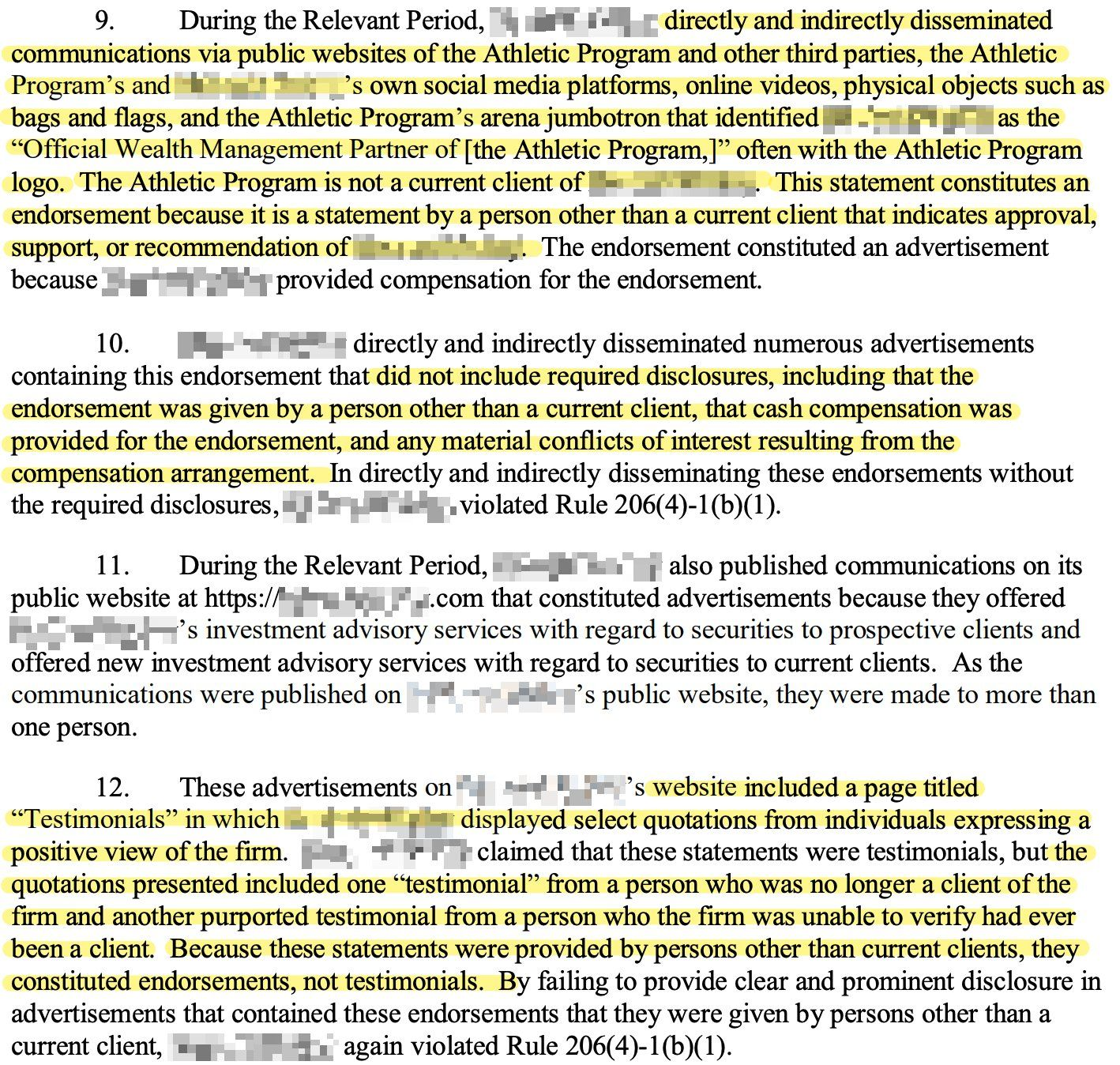

Third-party ratings and testimonials compliance: the SEC is not messing around

As evidenced by the SEC’s most recent enforcement sweep, the SEC is strictly enforcing compliance with the Marketing Rule and, more specifically, the disclosure requirements to use third-party ratings and testimonials.

If an RIA references a third-party rating in its advertisements (e.g., XYZ’s Top 100 Advisors), be sure to clearly and prominently disclose:

✅ The date on which the rating was given

✅ The period of time upon which the rating was based

✅ The identity of the third-party that created/tabulated the rating

✅ If applicable, that compensation was directly or indirectly paid by the RIA in connection with obtaining or using the third-party rating

Also remember that a testimonial is given by a current client, and an endorsement is given by anyone other than a current client.

If an RIA references a testimonial or endorsement in its advertisements, be sure to clearly and prominently disclose:

✅ That the testimonial was given by a current client or the endorsement was given by someone other than a current client

✅ If applicable, that cash or non-cash compensation was provided for the testimonial and endorsement

✅ A brief statement of any material conflicts of interest on the part of the person giving the testimonial or endorsement

Remember to correctly distinguish between a testimonial and endorsement. If a client previously provided a testimonial and is no longer a client, what was once a testimonial is now an endorsement.

Finally, remember that no RIA is “conflict free,” as the SEC states in no uncertain terms that there are certain conflicts of interest “inherent” to a firm’s role as an investment adviser. No advertisement should assert that an RIA is free from conflicts of interest.

The screenshots below are examples from the recent enforcement sweep of what not to do.

Did you know you can self-monitor your IAR Continuing Education progress with a FinPro Account?

As you may be aware, certain states have adopted an annual Investment Adviser Representative (“IAR”) Continuing Education (“CE”) requirement. The states that have adopted an IAR CE requirement can be reviewed here, but have also been copied below for ease of reference as of December 12, 2024:

- Arkansas (effective in 2023)

- California (effective in 2024)

- Colorado (effective in 2024)

- Florida (effective in 2024)

- Hawaii (effective in 2024)

- Kentucky (effective in 2023)

- Maryland (effective in 2022)

- Michigan (effective in 2023)

- Minnesota (effective 1/1/2025)

- Mississippi (effective in 2022)

- Nebraska (effective 1/1/2025)

- Nevada (effective in 2024)

- New Jersey (effective in 2025)

- North Dakota (effective in 2024)

- Oklahoma (effective in 2023)

- Oregon (effective in 2023)

- Rhode Island (effective in 2025)

- South Carolina (effective in 2023)

- Tennessee (effective in 2024)

- Vermont (effective in 2022)

- Washington, D.C. (effective in 2023)

- Wisconsin (effective in 2023)

- U.S. Virgin Islands (effective in 2025)

Such IAR CE requirements apply equally to both registered IARs of state-registered investment advisers and SEC-registered investment advisers, and is based on where the individual IAR is registered (not necessarily where the investment adviser firm is registered or notice filed). Thus, if you are an IAR that is individually registered in one of the states listed above that had an IAR CE requirement in effect for 2024 or earlier, you are required to attain 12 IAR CE credits before December 26th – the date that the IAR CE reporting system shuts down for the year. The 12 IAR CE credits must include 6 credits of Products and Practices and 6 credits of Ethics and Professional Responsibility.

The 2024 IAR CE deadline of December 26th is quickly approaching. All IAR CE courses must be completed and reported by the IAR CE course provider to FINRA by December 26th in order for credits to be applied before January 2nd. When the CRD system shuts down on December 26th, IAR CE statuses will be set based on credits reported in the system at that time.

To self-monitor your IAR CE, review your IAR CE transcript, or view your IAR CE requirement status, login to your FinPro account. Don’t have a FinPro account yet? Create one here.

For further resources, please refer to the NASAA IAR CE Resource Page, FAQs, Program Information, and the list of Approved IAR CE Providers.

The scale of ‘off-channel communications’ penalties handed down by the SEC since 2021 is pretty staggering – $2 billion collected from over 100 firms

In a recent speech (as excerpted in the annotated screenshot below), the Acting Director of the SEC’s Division of Enforcement shared the factors that are considered by Enforcement Staff when assessing the penalty to recommend.

The takeaway for RIAs? Communications that fall under the SEC’s Recordkeeping Rule (whether via email, text, DM, carrier pigeon, etc.) should either be retained in the firm’s records or not communicated in the first place. Policies/procedures, personnel training, and periodic testing should go a long way in battening down the hatches.

Out of curiosity, I asked ChatGPT, Perplexity, Claude, and Gemini a question that I’m commonly asked:

Does state XYZ require a solicitor/promoter to be registered as IAR?*

👌🏻 One provided the correct answer and cited the state’s statutory exception.

👎🏻 Two provided the incorrect answer.

🤷 One pretended it was an attorney and more or less responded with “it depends”.

*This was not the full prompt; I added additional context, suggested what sources to review, etc.

My takeaway is that while AI chat tools may provide some preliminary directional assistance, there is not yet a replacement for reviewing the actual source materials themselves.

It also doesn’t help that some states are, shall we say, less than transparent with respect to their “informal expectations” that are not always memorialized in public writings.

SEC Chair Gensler to depart on January 20, 2025; former SEC Commissioner Paul Adkins nominated as the new SEC Chair

I suppose outgoing Chair Gensler’s imminent departure shouldn’t come as a surprise (read the full press release here).

The newly-nominated (though not confirmed) SEC Chair – Paul Adkins – should hopefully bring some much-needed scrutiny of newly-proposed and recently-adopted regulations and will likely bring a more crypto-friendly perspective to the SEC (background article here).

Seeking Best Execution: Understanding The SEC’s Expectations For Advisors To Deliver Best Outcomes For Clients

An investment adviser is a fiduciary. As a fiduciary, an investment adviser owes a duty of care and loyalty to its clients. The duty of care obligates an investment adviser to seek best execution of client securities transactions.

Easy, right?

If only.

Neither the Investment Advisers Act of 1940 nor any of the rules promulgated thereunder contain a single reference to the term “best execution”. Nor do the General Instructions to Form ADV or Form ADV Part 2. To decipher the SEC’s expectations with respect to best execution, an adviser must traverse a path through the fiduciary of care and loyalty, borne from a Supreme Court case dating back to 1963, an SEC interpretive release from 1986, an SEC Risk Alert from 2018, an SEC interpretation regarding an adviser’s standard of conduct from 2019, and (of course) various enforcement actions over the years.

Best execution is even more of an enigma for advisers that manage client accounts through a single executing broker-dealer that also serves as the qualified custodian of the assets maintained in client accounts (what we’ll simply refer to herein as a “custodial broker-dealer”). Advisers that otherwise limit the number of custodial broker-dealers through which they execute trades to those directed by clients face a similar quandary. And given that most blue-chip custodial broker-dealers have effectively eliminated trading commissions for US equities and certain other products, comparing the actual execution costs among such firms may seem like performative quibbling rather than substantive analyses.

My latest article is an attempt to unpack an adviser’s fiduciary duty to seek best execution of client securities transactions, and what substantive actions can be taken to comply with SEC expectations in this regard.